Fundamental theory

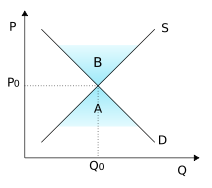

The intersection of supply and demand curves determines equilibrium price (P0) and quantity (Q0).

Strictly considered, the model applies to a type of market called perfect competition in which no single buyer or seller has much effect on prices and prices are known. The quantity of a product supplied by the producer and the quantity demanded by the consumer are dependent on the market price of the product.

The law of supply states that quantity supplied is related to price. It is often depicted as directly proportional to price: the higher the price of

the product, the more the producer will supply, ceteris paribus. The law of demand is normally depicted as an inverse relation of quantity

demanded and price: the higher the price of the product, the less the consumer will demand, cet. par. "Cet. par." is added to isolate the effect of price. Everything else that could affect supply or demand except price is held constant. The respective relations are called the 'supply curve' and 'demand curve', or 'supply' and 'demand' for short.

the product, the more the producer will supply, ceteris paribus. The law of demand is normally depicted as an inverse relation of quantity

demanded and price: the higher the price of the product, the less the consumer will demand, cet. par. "Cet. par." is added to isolate the effect of price. Everything else that could affect supply or demand except price is held constant. The respective relations are called the 'supply curve' and 'demand curve', or 'supply' and 'demand' for short.

The laws of supply and demand state that the equilibrium market price and quantity of a commodity is at the intersection of consumer demand and producer supply. Here, quantity supplied equals quantity demanded (as in the enlargeable Figure), that is, equilibrium. Equilibrium implies that price and quantity will remain there if it begins there. If the price for a good is below equilibrium, consumers demand more of the good than producers are prepared to supply. This defines a shortage of the good.

A shortage results in the price being bid up. Producers will increase the price until it reaches equilibrium. If the price for a good is above

equilibrium, there is a surplus of the good. Producers are motivated to eliminate the surplus by lowering the price. The price falls until it

reaches equilibrium.

equilibrium, there is a surplus of the good. Producers are motivated to eliminate the surplus by lowering the price. The price falls until it

reaches equilibrium.